Modules of Private Equity Investors

- Who can be a PEI

- How an investor works

- How the regulation works for PE

- The remuneration of PE

Overview

The Formats

- The European Union format: This format is regulated by a Directive of the European Union.

- two Directives regulating PE activity: The Banking Directive & The Financial Services Directive

- The Anglo-Saxon format: This format is regulated by US and UK laws.

- In the Anglo-Saxon world, PE is not a financial service (as it is in Europe), rather it is an entrepreneurial activity.

The European Union World

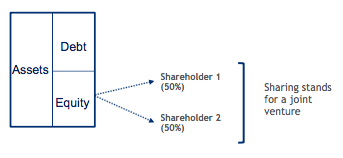

Three vehicles can be a PEI in Europe

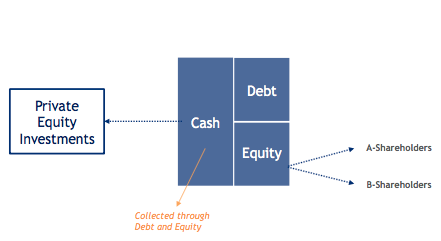

- Closed-End Funds - most suitable player

- Asset Management Company (AMC)

- Closed-End Fund

- Investors

- Banks

- Investment Firms

Notes: Closed end funds have a fixed maturity and a fixed amount of money to invest.

Rules

For the AMC, the set of rules concerns:

- Minimum requirements to operate

- Governance rules

- Management rules

For the funds, the set of rules concerns:

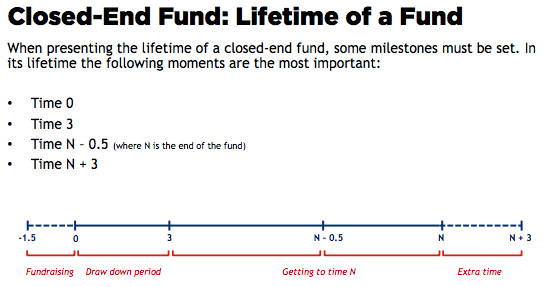

Lifetime of a Closed-End Fund in Europe

Fundraising - Draw Down Period - Getting to Time N - Extra Time

- Year 0-3: first investment

- Year 3-5: exit from the first investment

- Year 5-7: second investment

- Year 7-10: exit from the second investment

Management Fees and Carried Interest

Management Fees

- The management fees is a fixed percentage of money calculated on the value of the closed-end fund in the beginning of the fund itself.

Carried Interest

- Maximizing the carried interest is the ultimate goal and desire of an AMC.

- CARRIED INTEREST = % x (Final IRR – Hurdle IRR)

- The fixed percentage - 25-30%; the hurdle rate - 7-8%

Investment Firms and Banks in Europe

Banks

Banks have to follow very strict constraints and rules.

Investment firms

- A-shareholders: act as an AMC. management fees + a yearly carried interest

- B-shareholders: profits - the carried interest given to A-shareholders

Investment firms can undertake the same activity as banks with the exception of collecting money through deposits.

The Anglo-Saxon World

In the Anglo-Saxon markets, it’s can be noted that investments in PE are not regulated by a regulation framework, rather they are market-related - the market discipline is more powerful and important than a financial authority regulation.

That means PE investment is considered a business activity and not a financial activity as it is in Europe.

PE Players in the US

- Venture Capital Funds (VCFs, funds - most popular)

- Small Business Investment Companies (SBICs)

- Banks

- Corporate Venture

- Business Angels

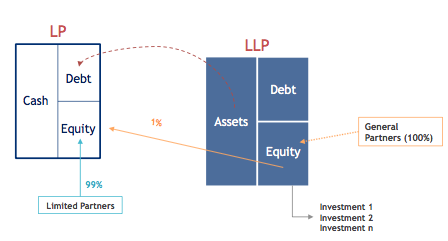

Limited Partnerships in the US

A fund is just simply a common pool, that means a bank account in which investors put money to be managed all together.

Limited partnership (LP): An LP is one of the typical structures to create a company in the US, whereas common organizational forms are: sole proprietorship, partnership, limited-liability partnership, limited partnership, S-corporation and C-corporation. LPs generally are private investors, banks, pension and insurance funds, and corporate investors; and they are allowed to leverage.

Shareholders: the LPs - 99% of the equity of the LP - investors || the General Partners (GPs) - 1% of the entity of the LP - managers

- Europe:a code - a legal battle; a Supervisor || US - a contract, a Limited Partnership Agreement; a Court

- Europe:AMCs, managers; VCFs, investors|| US - GPs, LLP, managers; LPs, investors

The great success of LPs is due both to

- 1) the simple scheme of functioning and

- 2) to the tax transparency - taxes = 0% for a PE investment.

The regulatory framework of Anglo-Saxon Format

PE is not a financial service (as it is in Europe), rather it is an entrepreneurial activity, and there is no supervisor.

SBIC in the US

SBIC

- the Small Business Investment Company

- two shareholders: a US Public Admin; pure investors; mangement fees + a threshold stated in the SBIC Agreement || the non-public admin investors, a bank, corporation, individual; managers; mangement fees + all the rest of the profits > 50% shares

- 33% of debt, a very low and fixed rate

- the best models of PPPs (Public-Private Partnerships)

Corporate Ventures

Not legal entities, promote R&D, outputs, enhance the value for the corporation

Business Angels

QSBS rule - Qualified Small Business Stock rules, taxes benefits for the seed and start-up financing

Banks

Rare - many constrains

Funds and VCTs in the UK

- Venture capital funds (VCF)

- Venture capital trusts (VCT)

- Banks

- Business Angels

- Local PPPs

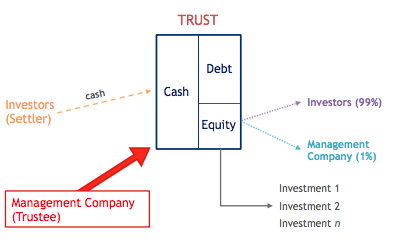

Venture Capital Trust

A trust is a very old British institution (there is evidence of the first trusts in the 11th and 12th century) and it is an entity, not a company. The trust was born in the first place for succession issues, as a matter of fact through this mechanism the owner (called the settlor) does not have to manage the assets, for a third player will do it (the trustee) and that is fully liable. In case the VCT has a maturity, at the end of the VCT the owner gets back the assets belonging to the trust.

Investors; Settlors || Managers, Management Company; Trustee

Taxation

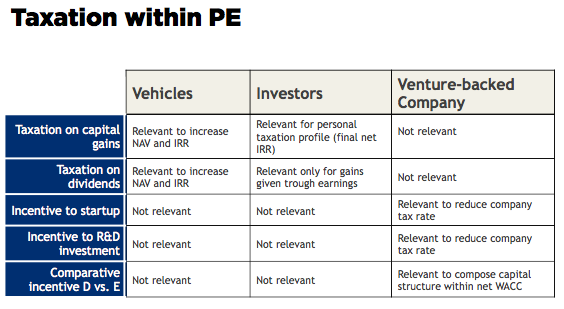

Taxation within PE

Taxation on Capital Gains for the VEHICLES

Participation Exemption (PEX) - a threshold, lower

Flat tax: It works like the PEX, only without any conditions. The tax rate is lower that the tax rate in the country (like for Close-end Funds in Europe for which the tax rate is 20%).

Tax Transparency:

Taxation on Capital Gains for the INVESTORS

Taxation on Dividends

The same rules as the capital gains

Incentives to R&D and Startups

- Mark Down: 3 years tax 0%

- Shadow Costs

- Tax Credit

Taxation and Incentives to D/E Ratio

- Thin Cap

- Double Income Taxation