The Managerial Process for Equity Funds

The managerial process is the day-by-day activity of the managers managing the investment made by the investors. When highlighting the characteristics of the managerial process, both academia and practitioners consider this process as made up of four steps:

- Fundraising - 1.5y in EU vs 1y in US

- Investment activity - evaluation & managment

- Managing and Monitoring - ensure the creation of value

- Exiting - most important by generating a capital gain

The exiting moment is in the end the reason why managers do PE activities, that is they have to understand when (and if) they will be able to exit.

Fundraising

Fundraising is a selling game about the business idea in which reputation, mutual trust, and love for risk are the pillars. The proposal is basically a business idea that leads to the creation of a vehicle to invest in private equity to produce value that will be spread among the promoters- managers and the investors.

The typical fundraising activity steps are as follows:

- Business Idea Creation

- Job Selling

- Raising Debt

- Closing

Business Idea Creation

The information memorandum has to explain the rationale of the business idea which is strictly linked to the reputation and to the track record of the promoter to the business community

Internal code of activity in EU vs LPA's contract in US

Job Selling

The letter of commitment via one-to-one meetings between the promoters and the potential counterparts

Debt Raising

Only accurs in the US and in the UK

The goal is to sell a project to a community of financers and it is difficult for each counterpart (the investors and the banks) to make the first move. Still the reputation is important.

Closing

A "successful" closing occurs based on it reputation and the purpose of the initiative or a "pure" closing without any money collection.

Investing: The Decision Making Phase

Investing involves in two different important moments:

- Decision-Making: valuation and selection

- Deal-Making: negotiation of the contracts about the rules

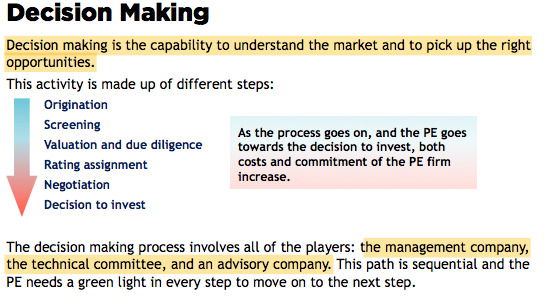

Decision Making

Decision making is the capability to understand the market and to pick up the right opportunities, involving in the the management company, the technical committee, and an advisory company.

Origination

The PE must decide the destination of the money collected, and scout the market.

Screening

100/10/1 rule in startup

Managers + Technical committee

Due Diligence and Valuation

The analysis of the business plan - long time

Rating Assignment

Assess the level of risk and understand the debt

Negotiation

The negotiation with the entrepreneur to calculate the numbers of shares a PE owns and the stake

Decision to Invest

The managers: the GPs vs the directors in an AMC in EU

The beginning of the second part of the investing phase: Deal making.

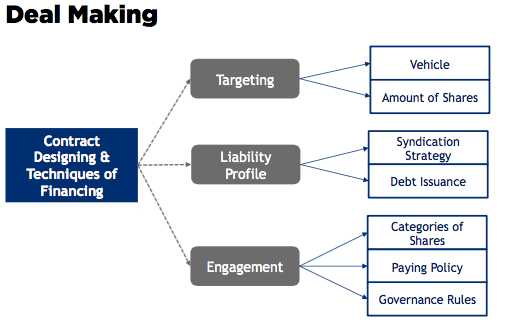

Investing: The Deal Making Phase

The deal making activity is related to the financial and legal issues related to the investment in the venture-backed company, finding the right balance between the need of money of the company and the expectation of IRR and capital gain for the PE investors.

Finding the right balance is not easy and the whole process is based on three pillars:

- Targeting

- Liability profile

- Engagement

Deal Making flow

Targeting

1. The Vehicle

A direct investment or in an indirect investment with the SPV - convincing the banking system

2. The Amount of Shares

Majority versus minority, Relative and absolute size of investment, Capital requirement impact, Voting rights and effective influence within the board of directors

Liability Profile

The Syndication Strategy

Share the risk borne otherwise only by the PE firm

Debt Issuance

A very hands-on approach towards the venture-backed company, involving the negociation with the banking system

Engagement

The PE firm has to set up the rules by which a PE can govern the venture-backed company.

Categories of Shares

Typical choices: Common shares, Shares with limited or increased rights, Shares with embedded option: for instance a share with a put option allowing the PE to sell the shares under some particular circumstances, Tracking stocks

Paying Policy

To address related to the fact that a PEI is buying another company’s shares.

The main activity of a PEI is to finance a company.

Governance Rules

Numbers of directors, Can the PEI sitting on the board of directors, The scheduling of the board meetings

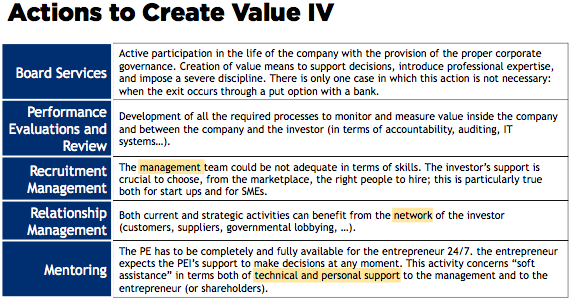

Managing and Monitoring: Supporting the Company

Managing & Monitoring

- Actions to create and to measure value

- Rules to protect the created value

Enhance the value of the company(shareholders + investor)

The nature of this presence depends on:

- The stage of the investment

- seed and start up: industrial and strategic

- expansion and replacement: financial and legal issues

- The style of the investor and the nature of the investment agreement

- The hands-on approach: financial and strategic decisions

- The hands-off approach: financial decisions

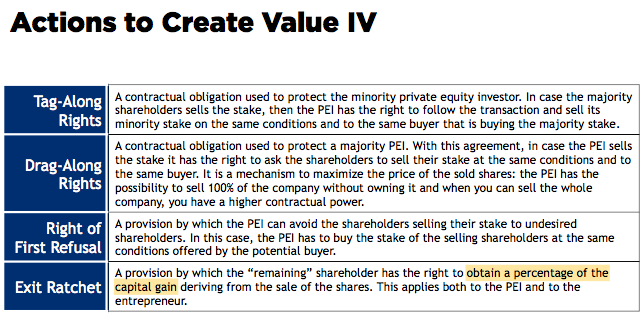

The key activities to create value

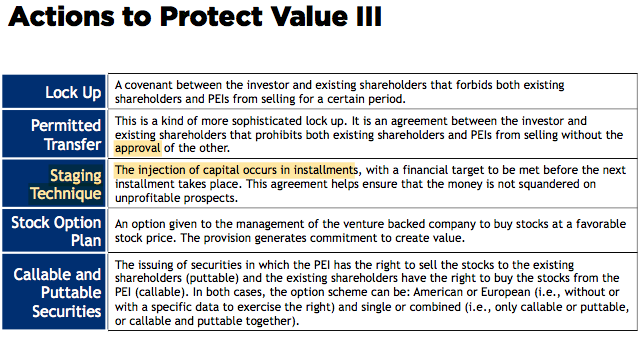

Managing and Monitoring: Covenants Usage

Protect the divergence of opinions between the entrepreneur and the PEI and the risk of struggle that may derive from it.

The typical covenants

Exiting

Exiting is the most difficult step for a PEI, because there exists both a pricing and a liquidity issue.

Exiting strategies have to be contextualized according to the portfolio strategy of the PEI. There is in fact a double perspective where the IRR of the investment has to be coordinated with goals and constraints coming from the whole portfolio.

Note: Theory and market trends show there is no correlation between: the stage of investment, the holding period and the exit way strategy.

The typical exiting strategies are the following:

- Trade sale

- Buy back

- IPO or sale post IPO

- Sale to other private equity investors 5. Write off

1. Trade Sale

- Based on the industrial relation

- Not very widespread

- Common in LBO, the PE holds the drag along right & in PIPEs

2. Buy Back

This option to exit gives for granted the fact that the entrepreneur has got liquidity enough to buy the shares.

One of the most used covenants in these cases is the puttable shares.

3. IPO

- The best option a PEI could ever dream of. I

- A PEI can maximize the capital gain

- Only in 1% of the cases

- Saling its stake in the stock exchange

- Difficult but must be ready for it "bubbles"

4. Sale to Another Private Equity Investor

Common in the American market and is based on strong relationship between PEI and the community of PEIs.

5. Write Off

The worst nightmare of a PE

Private Equity Advice for Entrepreneurs

The chemistry and the personal relation between the PE and the entrepreneur is fundamental to make the partnership successful. —— Prof. Fabio Sattin